Ever stared at an insurance application wondering which boxes to check and whether you’re about to overpay for coverage you don’t actually need?

Quick answer: Food truck insurance is a combination of commercial policies — typically general liability, commercial auto, and workers’ compensation — that protects your mobile food business from accidents, lawsuits, equipment damage, and food-related claims. Most food truck owners pay roughly $2,000 to $4,000 per year for a solid set of coverages, though your costs depend on what you serve, where you operate, and how many people you employ.

I remember sitting in my truck after my first big event, realizing that if someone had slipped on the wet pavement near my serving window, I’d have been personally on the hook for every dollar. That was the moment I stopped treating food truck insurance as “something I’d figure out later.”

One important note: I’m not an insurance agent or attorney. This guide reflects my experience as a food truck owner and mentor — not professional insurance advice. Always verify your specific requirements with a licensed insurance professional in your state.

This guide breaks down every coverage type, real cost ranges, and the decision framework I wish someone had given me before I signed my first policy.

📚 Part of our complete Food Truck Permits and Licenses guide.

So What Exactly Is Food Truck Insurance?

Food truck insurance isn’t one single policy — it’s a set of commercial insurance coverages designed specifically for the risks that come with running a mobile food business. Think of it as a safety net that catches everything from a fender bender on the way to a lunch spot to a customer who claims your food made them sick.

Here’s the thing: your personal auto insurance won’t cover your truck when it’s being used for business. Your homeowner’s policy won’t cover the commercial griddle that catches fire. And if an employee slices their hand during prep, your personal health plan isn’t going to handle that either.

Food truck insurance fills every one of those gaps.

What makes this type of coverage unique is that you’re dealing with overlapping risk categories all at once. You’re a restaurant, a commercial vehicle, an employer, and sometimes an event vendor — all rolled into one operation. That’s why most food truck owners need multiple policies working together, not just a single plan.

💡 Pro Tip from Jo: Get at least three food truck insurance quotes before committing. I learned the hard way that quotes can vary by hundreds of dollars for the exact same coverage.

📎 Related: Learn what business licenses for food trucks your state requires alongside insurance.

What Types of Food Truck Insurance Does Your Business Actually Need?

Okay, I know this next part feels like a lot. But stay with me — once you understand what each coverage type actually does, you’ll feel way more confident when you’re comparing policies.

The types of food truck insurance you need depend on your specific operation, but most owners carry at least three core coverages. Here’s the breakdown.

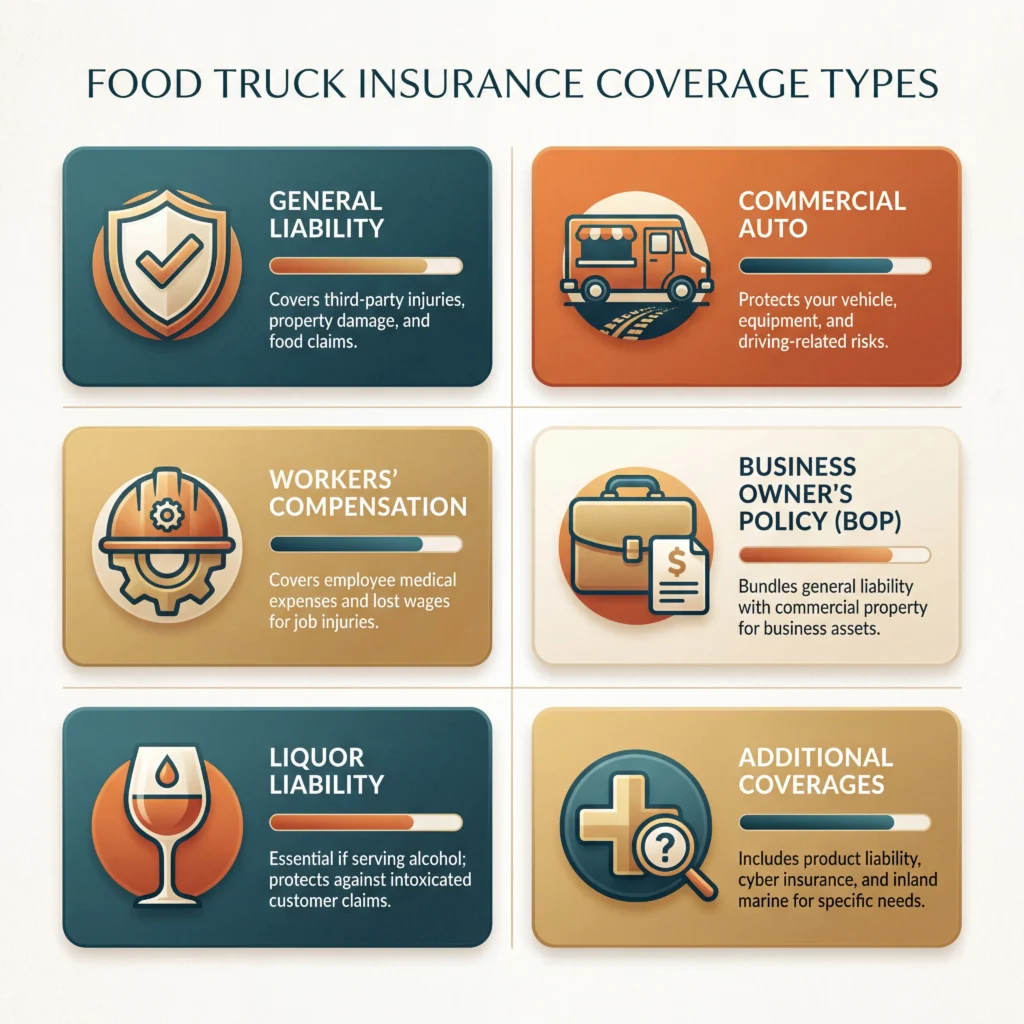

General Liability Insurance

This is the foundation. General liability covers you when a customer gets hurt near your truck, when someone claims your food made them sick, or when you accidentally damage property at a venue. Most policies provide $1 million per occurrence and $2 million aggregate.

Commercial Auto Insurance

Commercial auto is legally required in most states if you’re driving a vehicle for business purposes. It covers accidents on the road, vehicle theft, vandalism, and weather damage. Your personal auto policy will almost certainly deny a claim involving your food truck — don’t risk it.

Workers’ Compensation Insurance

Workers’ comp is required in most states the moment you hire your first employee. It covers medical expenses, rehabilitation, and lost wages if someone gets injured on the job. Kitchen injuries happen — burns, cuts, slips — and this coverage keeps both you and your team protected.

Business Owner’s Policy (BOP)

A BOP bundles general liability with commercial property coverage. It often protects your equipment — POS tablets, blenders, prep tables — even at a separate commissary kitchen. Many food truck owners find a BOP more affordable than buying general liability and property coverage individually.

Liquor Liability Insurance

If you serve alcohol, you need liquor liability. If an intoxicated customer causes harm after you serve them, you could be held personally liable. Many states have dram shop laws that specifically hold businesses accountable.

Additional Coverages Worth Considering

Product liability insurance protects against claims related to foodborne illness or allergic reactions. Some general liability policies include this, but check your terms carefully.

Inland marine insurance covers your portable equipment when it’s in transit — generators, serving equipment, and signage that moves between locations.

Cyber insurance is increasingly relevant if you process credit card payments. A data breach could expose customer information, and this coverage helps pay for notification costs and fraud monitoring.

I know that’s a lot of coverage types. You don’t necessarily need all of them — the next section helps you figure out exactly which ones matter for your situation.

📎 Related: If you’re just starting out, check our food truck permits guide to see what’s legally required before you can operate.

How Much Does Food Truck Insurance Really Cost?

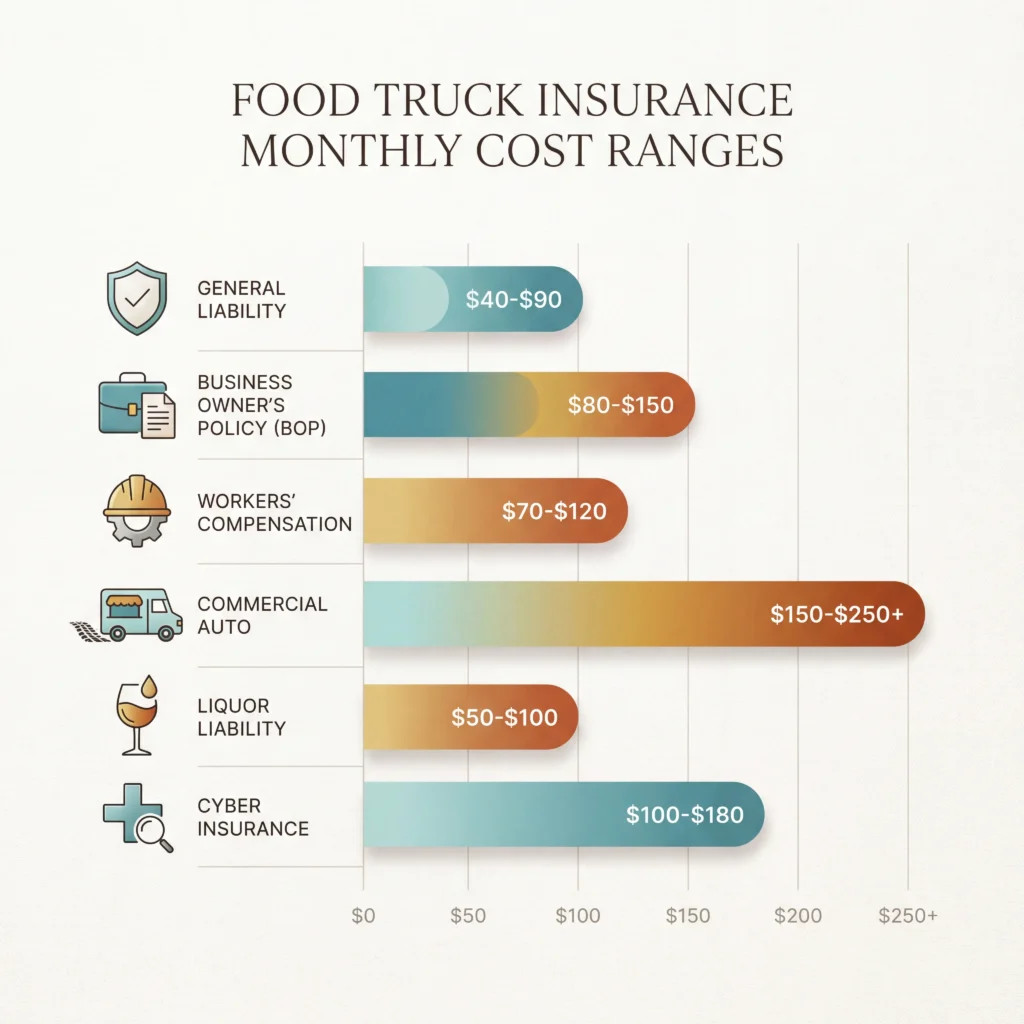

This is the question everyone asks, and most insurance company websites dodge it with “it depends.” I’m not gonna lie — it does depend — but here are real numbers to work with.

The following table shows median costs reported by food truck businesses through Insureon. Your actual rates will vary based on location, coverage limits, and business factors.

| Coverage Type | Avg. Monthly Cost | Avg. Annual Cost | Typical Limits |

|---|---|---|---|

| General Liability | $42/mo | ~$500/yr | $1M per occurrence / $2M aggregate |

| Business Owner’s Policy (BOP) | $84/mo | ~$1,008/yr | Varies by property value |

| Workers’ Compensation | $78/mo | ~$940/yr | State-mandated minimums |

| Commercial Auto | $170/mo | ~$2,041/yr | State minimum to full coverage |

| Liquor Liability | $58/mo | ~$700/yr | $1M per occurrence / $2M aggregate |

| Cyber Insurance | $145/mo | ~$1,740/yr | Varies |

Source: Median premiums from Insureon food truck customer data. Rates reflect their most recently published figures and may have been updated since. Always request current quotes from providers.

For a typical food truck owner carrying general liability, commercial auto, and a basic BOP, adding up these medians gives you roughly $296 per month in total food truck insurance costs. That’s a real line item in your budget, but it’s far less than a single lawsuit would cost you out of pocket.

Several factors push your premiums higher or lower. The type of food you serve matters — a truck running a deep fryer and grill will typically pay more than one making cold sandwiches. Where you operate plays a role too, since states and cities vary widely in their liability environments. Your claims history, the value of your truck and equipment, employee driving records, and the policy limits and deductibles you choose all factor in as well.

Real talk: $1,000,000 in general liability coverage typically runs food truck owners between $30 and $85 per month, depending on those variables. That’s the coverage level most events and venues require you to carry.

💡 Pro Tip from Jo: Ask your food truck insurance provider about bundling. When I combined my general liability and property coverage into a BOP, my total premium dropped compared to buying them separately. It’s not always cheaper, but it’s always worth asking.

📎 Related: Understanding insurance costs is part of knowing how much a food truck license costs overall.

How Do You Choose the Right Food Truck Insurance Quote?

Knowing what types of coverage exist is one thing. Knowing which ones you actually need — before you request your first food truck insurance quote — is where it gets personal.

Here’s the decision framework I wish someone had handed me on day one. Run through this checklist and check off what applies to your operation.

☐ Do you drive your truck on public roads? → You need commercial auto insurance. Non-negotiable and legally required in nearly every state.

☐ Do you have employees? → You need workers’ compensation. Most states require it the moment you have even one employee. Check your state’s labor department website for specifics.

☐ Do you serve food to the public? → You need general liability with product liability coverage. This protects you against slip-and-fall claims and foodborne illness lawsuits.

☐ Do you serve alcohol? → Add liquor liability. Dram shop laws in many states can hold you personally responsible for damages caused by an intoxicated customer you served.

☐ Do you own expensive equipment? → A BOP or inland marine policy protects that investment. Think about what it would cost to replace your most expensive piece of equipment overnight — that number tells you whether this coverage is worth it.

☐ Do you accept credit cards? → Consider cyber insurance. A data breach hits small businesses harder than big ones because you don’t have a legal team on standby.

☐ Do you work events, festivals, or private catering? → You’ll need the ability to add additional insureds to your policy quickly. Some providers make this free and instant online. Others charge per addition and take days. Ask about this before you buy a policy.

And here’s what this framework really gives you: clarity on what you don’t need. If you’re a solo operator who doesn’t serve alcohol, you could skip workers’ comp and liquor liability — potentially saving over $130 per month. That’s money back in your business.

When I was in your shoes, I made the mistake of just buying the cheapest policy I could find without actually reading what it covered. Turned out my “general liability” didn’t include product liability — which meant foodborne illness claims weren’t covered. I only found out when a mentor asked me to check. Don’t be me. Read the policy terms before signing.

Does Your State Have Special Food Truck Insurance Requirements?

Food truck insurance requirements aren’t uniform across the country. What you need in California looks quite different from what’s required in Texas or Florida, and cities within the same state can add their own layers.

Most states require commercial auto insurance with minimum liability limits, but those minimums vary significantly. Here are a few examples to illustrate the range:

- Texas: Minimum commercial auto liability of $30,000 per person / $60,000 per accident / $25,000 property damage

- California: Minimum of $15,000 per person / $30,000 per accident / $5,000 property damage

- Florida: Requires PIP (Personal Injury Protection) coverage in addition to liability minimums

- New York: Higher minimums at $25,000 per person / $50,000 per accident / $10,000 property damage

Beyond state law, your local health department, city permitting office, and commissary kitchen may each require proof of specific coverages. Many cities require a Certificate of Insurance (COI) showing at least $1 million in general liability coverage just to get a mobile food vendor permit.

Here’s where it gets interesting: some of the most food-truck-friendly states — like Texas and Florida — have relatively straightforward insurance requirements, while states with complex permitting (I’m looking at you, Pacific Northwest) often have additional layers of required coverage.

My recommendation: before you buy any food truck insurance policy, call your city’s health department, your county clerk’s office, and any commissary kitchen you plan to use. Ask each one exactly what insurance documentation they require. You can also check your state’s Department of Insurance website for current minimums.

You don’t want to discover a missing requirement on the day you planned to launch.

📎 Related: Our guide to food truck regulations covers the legal landscape beyond just insurance.

What About Food Truck Insurance for Events and Festivals?

If events and festivals are part of your business model — and for many food truck owners, they’re the most profitable days of the year — you need to understand how insurance works in that context.

Most event organizers will require you to provide a Certificate of Insurance (COI) before they’ll approve your application. A COI is a one-page document from your insurance company that proves you carry the required coverage. It’s not a separate policy — it’s just proof of your existing food truck insurance.

Here’s the thing that catches people off guard: many events also require you to name the event organizer as an “additional insured” on your policy. This means your liability coverage extends to protect them if something goes wrong at your truck during their event.

Some insurance providers add additional insureds for free through an online portal. Others charge a fee each time. I’ve worked with providers who made it instant and free, and others who charged $25 per addition and took three business days. That difference matters when an event organizer needs your COI by tomorrow.

When you’re comparing food truck insurance quotes, ask specifically: “How do I add an additional insured, how fast is it, and does it cost extra?” If you’re doing multiple events per month, these fees add up.

💡 Pro Tip from Jo: Keep a digital copy of your COI on your phone at all times. I’ve been asked for proof of insurance during health inspections, at farmers market check-ins, and even by random city inspectors who stopped by my truck. Having it ready saves you stress and makes you look professional.

📎 Related: If catering events is a big part of your plan, check out our food truck catering guide.

Food Truck vs. Food Trailer: Is the Insurance Different?

Yes, and the distinction matters more than you’d think.

A food truck is a self-propelled vehicle with a built-in kitchen. A food trailer is towed behind a separate vehicle. Because of that difference, your food truck insurance needs change significantly.

Food trucks need commercial auto insurance — the truck itself is both your vehicle and your kitchen. One policy covers the driving risks and often the permanently attached equipment.

Food trailers aren’t self-propelled. Your standard general liability policy may not automatically cover incidents involving the trailer when it’s detached and parked at an event. Some providers offer a specific food trailer endorsement that extends your liability coverage to the trailer when it’s stationary and disconnected from your tow vehicle. Not all providers offer this, so ask specifically.

You’ll also need a separate auto policy for whatever vehicle tows the trailer. If you’re using a personal truck to tow a commercial food trailer, your personal auto policy probably won’t cover a towing accident during business use. You may need either a commercial auto policy for the tow vehicle or a hired and non-owned auto (HNOA) policy.

Can we talk about how confusing this is? When I first started researching trailer insurance, I thought it would be simpler than insuring a full food truck. It’s actually more complicated because you’re dealing with two separate assets — the trailer and the tow vehicle — instead of one integrated unit.

📎 Related: For a deeper dive beyond insurance, see our food truck vs. food trailer comparison.

The Food Truck Insurance Mistakes I See Owners Make

After mentoring over a dozen food truck owners through their first year, I see the same insurance mistakes come up again and again. Here’s what to watch out for.

Mistake #1: Using Personal Auto Insurance for a Commercial Vehicle

Your personal policy will almost certainly deny any claim that happens while you’re using your vehicle for business. If you get into an accident driving to a lunch spot, your personal insurer has every right to say “this is a commercial vehicle, claim denied.” Get commercial auto coverage — no exceptions.

Mistake #2: Buying the Cheapest Policy Without Reading the Terms

I’ve seen owners buy a general liability policy only to discover it excluded product liability — meaning food-related illness claims weren’t covered. The food truck insurance policy that’s $20 cheaper per month might be missing the one coverage you actually need.

Mistake #3: Not Getting Enough Coverage to Meet Venue Requirements

I watched a fellow food truck owner lose a profitable weekend festival booking because their policy had a $500,000 limit instead of the $1 million the organizer required. They’d saved about $15 per month on premiums — and lost ten times that in one weekend. Know the coverage requirements in your market before you buy.

Mistake #4: Forgetting About Equipment That’s Not Permanently Attached

Your commercial auto policy typically covers equipment bolted to the truck. But what about your portable generator, your pop-up tent, your signage? If it’s not permanently attached, it may not be covered unless you have inland marine or a BOP with business personal property coverage. Inland marine policies vary widely in cost depending on your equipment value — ask your provider for a specific quote.

Mistake #5: Not Updating Your Policy as Your Business Grows

You hired two employees but didn’t add workers’ comp. You started serving alcohol but didn’t add liquor liability. You upgraded your truck but didn’t update your property values. Your food truck insurance should grow as your business grows. Review your coverage at least once a year.

What Happens If You Actually Need to File a Claim

One more thing worth knowing: if you ever do need to file a claim, the process is usually straightforward. Contact your insurance company’s claims department, provide documentation of the incident — photos, written statements, medical records, or police reports if applicable — and a claims adjuster will review your case.

Most food truck claims are resolved within 30 to 90 days. Having your policy number, a written incident summary, and supporting documentation organized ahead of time speeds everything up. I keep a folder on my phone specifically for this — photos of my truck, equipment serial numbers, and my policy documents. You hope you never need it, but you’ll be grateful if you do.

Putting It Into Practice

📅 Today: Call your city’s health department and ask which insurance documents they require for a mobile food vendor permit.

📅 This Week: Request food truck insurance quotes from at least 3 providers. Compare coverage types and limits — not just monthly prices. Ask each one how they handle additional insureds for events.

📅 This Month: Have your policies active, your COI saved digitally on your phone, and your first event application submitted with proof of coverage.

FAQ: Your Food Truck Insurance Questions, Answered

How much does food truck insurance cost per month?

Most food truck owners pay between $200 and $400 per month for a solid combination of general liability, commercial auto, and either a BOP or additional property coverage. Some food-industry-specialized providers offer basic general-liability-only policies starting around $25 to $30 per month, but that won’t cover your vehicle, your equipment, or your employees. Your actual cost depends on what you serve, where you operate, your claims history, and how many people you employ.

What is the best insurance for a food truck?

The best food truck insurance is the combination of policies that matches your specific operation — not necessarily the cheapest or the most well-known brand. At minimum, most owners need general liability, commercial auto, and workers’ comp if they have employees. Providers that specialize in food businesses often understand the unique risks better than general commercial insurers. Look for a provider that offers easy COI generation and fast additional insured processing if you work events.

Do I need food truck insurance if I only do a few events per year?

Yes. Even if you operate part-time or seasonally, you’re still exposed to liability every time you serve food to the public. Some providers offer short-term or event-based coverage if you don’t need a year-round policy, which can be more affordable for occasional operators. But don’t skip coverage entirely — one slip-and-fall claim or foodborne illness lawsuit can cost tens of thousands of dollars regardless of how often you operate.

What’s the difference between general liability and a business owner’s policy?

General liability covers third-party bodily injury, property damage, and advertising injury claims. A business owner’s policy (BOP) includes everything in general liability plus commercial property coverage — protecting your owned equipment, inventory, and sometimes even business interruption losses. A BOP typically costs about twice as much as standalone general liability, but it covers significantly more. For most food truck owners with valuable equipment, a BOP offers better overall value.

Can I get food truck insurance with no prior business experience?

Yes. Insurance providers don’t typically require business experience to issue a policy. You’ll need basic information about your business: what you plan to serve, where you’ll operate, the value of your truck and equipment, and how many employees you’ll have. Being a new business may mean slightly higher premiums since you have no claims history, but it won’t disqualify you from getting coverage.

Final Thoughts

Food truck insurance can feel like one more overwhelming line item on an already long startup checklist. But here’s what I’ve learned after going through it myself and watching others do the same: the owners who take insurance seriously from day one sleep better and recover faster when something goes wrong.

Quick Recap:

- Most food truck owners need at least general liability, commercial auto, and workers’ comp (if you have employees)

- Budget roughly $200 to $400 per month for a solid coverage combination based on current industry medians

- Always read the policy terms — the cheapest option may exclude the coverage you need most

- Your state, your city, and your event venues may each have different food truck insurance requirements

- Review and update your coverage at least once a year as your business changes

Ready to get covered? Start by requesting quotes from 2 to 3 providers. Many let you complete a food truck insurance quote online in under 10 minutes. Compare coverage types and limits — not just monthly prices — and make sure any provider you choose lets you add additional insureds easily if you work events.

Your Next Steps:

- Understand all the food truck permits and licenses you need in your area

- Check the food truck liability insurance details for a deeper dive on liability coverage

- Review mobile food truck insurance specifics if you’re comparing mobile vendor policies

- Get the full picture in our complete Food Truck Permits and Licenses guide

One last disclaimer: I’m not an insurance agent or lawyer — always verify requirements with a licensed professional in your state. But you’ve totally got this. Food truck insurance isn’t the fun part of running a food truck — but it’s the part that lets you keep doing the fun part.

— Jolene Matsumoto