Last Updated: February 6, 2026 | Rates Verified: February 6, 2026

Most food truck owners I meet make one expensive mistake when seeking their first food truck loan—they walk into the wrong lender asking for the wrong loan type.

Back in 2019, I sat in my bank’s parking lot for 45 minutes rehearsing my pitch before my second truck’s loan meeting. I’d spent six years on the other side of that desk evaluating small business loan applications. I knew exactly what killed deals.

That day, I watched a taco truck operator get declined 15 minutes before my appointment. Same loan amount I was requesting. Similar credit score. He walked out furious.

Here’s what he missed—and what changed everything for my application.

The 60-Second Answer: Which Food Truck Loan Gets You Funded Fastest?

Updated February 6, 2026 based on current market rates:

For most food truck purchases, SBA 7(a) loans offer the lowest rates (currently 9.75-14.75% as of January 2026, per NerdWallet) but take 60-90 days to approve.

If you need money in 10-15 days, equipment financing beats everything—14-20% rates with the truck as collateral.

If your credit is under 620, alternative online lenders approve in 48 hours but charge 18-35% APR.

The food truck loan you choose determines three things: your approval speed, your interest rate, and whether you’ll actually get funded. Based on my experience securing $180K across three trucks in San Antonio, here’s the system that works.

🎯 Download: Marcus’s Food Truck Loan Calculator

Free Spreadsheet Includes:

- Loan payment calculator for all 6 loan types

- Side-by-side lender comparison tool

- Document checklist (same one I used)

- Credit score impact simulator

Food Truck Loan Types: My Real-World Testing Results

When I expanded from truck #1 to truck #3, I evaluated 12 different food truck loan programs across seven lenders. Here’s what actually happened—not the marketing brochure version.

Updated February 6, 2026 with current market rates from Lendio, Bankrate, and the SBA.

| Loan Type | Amount Range | Rate (Feb 2026) | Approval Time | Credit Min | Marcus’s Reality Check |

|---|---|---|---|---|---|

| SBA 7(a) | $5K – $5M | 9.75-14.75% | 60-90 days | 650+ | Lowest rates but slowest. Worth it for trucks over $75K. I used this for truck #3. |

| Equipment Financing | $10K – $500K | 14-20% | 10-15 days | 620+ | Truck itself is collateral. Got my truck #2 funded in 12 days. My go-to for speed. |

| Business Line of Credit | $10K – $250K | 11-25% | 7-14 days | 650+ | Perfect for kitchen upgrades, not full truck purchases. Saved me during truck #1’s generator failure. |

| Alternative Lenders | $5K – $500K | 18-35% APR | 24-48 hours | 580+ | Expensive but they funded a friend when banks said no. Use only if desperate. |

| Microloans (SBA) | $500 – $50K | 8-13% | 30-45 days | 600+ | Great for your first small truck. Mission-driven lenders actually help. |

| Personal Loan | $1K – $100K | 9-36% | 24-72 hours | 640+ | I advise against this unless under $25K. Your personal credit takes the hit. |

Source Data: Prime rate 6.75% as of January 5, 2026 (Lendio). SBA maximum rates published monthly on SBA FTA wiki.

The Loan Type Nobody Told Me About

Equipment financing changed everything for my second truck.

Here’s what happened: I’d been preparing an SBA 7(a) application for three months. Business plan, projections, the works. My banker estimated 75-90 days to funding.

Then I met another food truck owner at a commissary who’d just bought a $78,000 truck. Funded in nine days.

His secret? He went straight to an equipment financing company. The truck was the collateral. Simple application. Fast approval. Rate was 16.2% vs the SBA’s 11.5% I was chasing, but he’d been running his truck for two months while I was still filling out forms.

I pivoted. Got approved in 12 days at 15.8%. Started generating revenue in week three. That revenue helped me qualify for better terms on truck #3 later.

The lesson: Perfect isn’t always profitable. Sometimes speed beats rate.

How Much Money Can You Actually Borrow for a Food Truck?

Lenders approved amounts that shocked me. Here’s the formula I learned from both sides of the desk.

The Real Lending Formula (From My Banking Days)

When I sat on the other side of the desk evaluating food truck loan applications, these are the exact calculations we ran:

Maximum Loan Amount = (Truck Value × LTV Ratio) + Working Capital

Where:

- LTV (Loan-to-Value) = 80-90% for new trucks, 70-80% for used trucks

- Working Capital = Usually 20-30% of truck cost for inventory/operations

Example from my truck #2:

- Truck cost: $65,000

- LTV at 80%: $52,000 toward truck

- Working capital approved: $13,000 (20% of truck cost)

- Total loan approved: $65,000

- My down payment: $13,000 (20%)

- Total project cost: $78,000

But There’s a Second Calculation Lenders Don’t Advertise

Debt Service Coverage Ratio (DSCR) killed more applications than bad credit in my banking days.

Formula: DSCR = Annual Net Operating Income ÷ Annual Debt Payments

Lenders want DSCR of at least 1.25. That means your business generates $1.25 for every $1.00 in loan payments.

My truck #3 example (the numbers I actually submitted):

- Projected annual income from truck #3: $142,000

- Annual operating expenses: $87,000

- Net operating income: $55,000

- Annual loan payment (at $65K loan): $17,124

- My DSCR: 3.21 (extremely strong)

This is why they approved me quickly. The numbers proved I could handle the debt.

New vs Used Food Truck Loan Amounts

New trucks ($50K-$175K):

- Banks love financing new trucks

- LTV up to 90% possible

- My truck #3 was new: got 85% LTV at 14.2% over 5 years

Used trucks ($20K-$85K):

- LTV drops to 70-80%

- Rates increase 1-3 percentage points

- But total project cost is lower—easier to manage

My recommendation based on 23 lending conversations: If you have strong credit (700+) and need a truck over $60K, buy new. The rate difference is negligible and approval is faster.

The Loan Officer’s Checklist Nobody Shows You

After six years in commercial banking and three food truck loan applications as a borrower, I know what actually matters in your file.

This is the checklist we used when evaluating food truck loan applications. Print this. Check every box before you apply.

What Loan Officers Actually Look At (In Order)

Priority 1: Cash Flow Ability

- [ ] DSCR above 1.25 (calculated from your financials)

- [ ] At least 6 months operating reserves shown

- [ ] Current business bank statements (they check average daily balance)

Priority 2: Credit Profile

- [ ] Personal credit score 650+ (they pull all three bureaus)

- [ ] No accounts in collections over $500

- [ ] Credit utilization under 40% on all cards

Priority 3: Down Payment Proof

- [ ] 10-20% down payment verified in bank account

- [ ] Funds seasoned at least 60 days (no sudden deposits)

- [ ] Paper trail if money came from family/gifts

Priority 4: Business Validation

- [ ] Business license active and current

- [ ] Health permits for your county (if existing business)

- [ ] Signed contracts or letters of intent from venues (for new businesses)

Priority 5: The Truck Itself

- [ ] Appraisal or NADA guide value (for used trucks)

- [ ] Equipment list with current values

- [ ] Photos of truck exterior and kitchen (seriously—we requested these)

The One Thing That Gets Overlooked

Time in business matters more than most people think.

Here’s what I learned: Lenders use operating history as a proxy for risk. Even if you have perfect credit, if you’re brand new, they’re nervous.

Workaround I used for truck #1 (when I had zero food truck history):

- Showed 6 years banking experience (relevant industry knowledge)

- Provided letter from commissary confirming my commercial kitchen rental

- Included signed contracts from two corporate lunch programs

- Added letters of intent from three regular event coordinators

Result: Approved despite being a startup. The documentation proved I wasn’t just dreaming—I had actual revenue lined up.

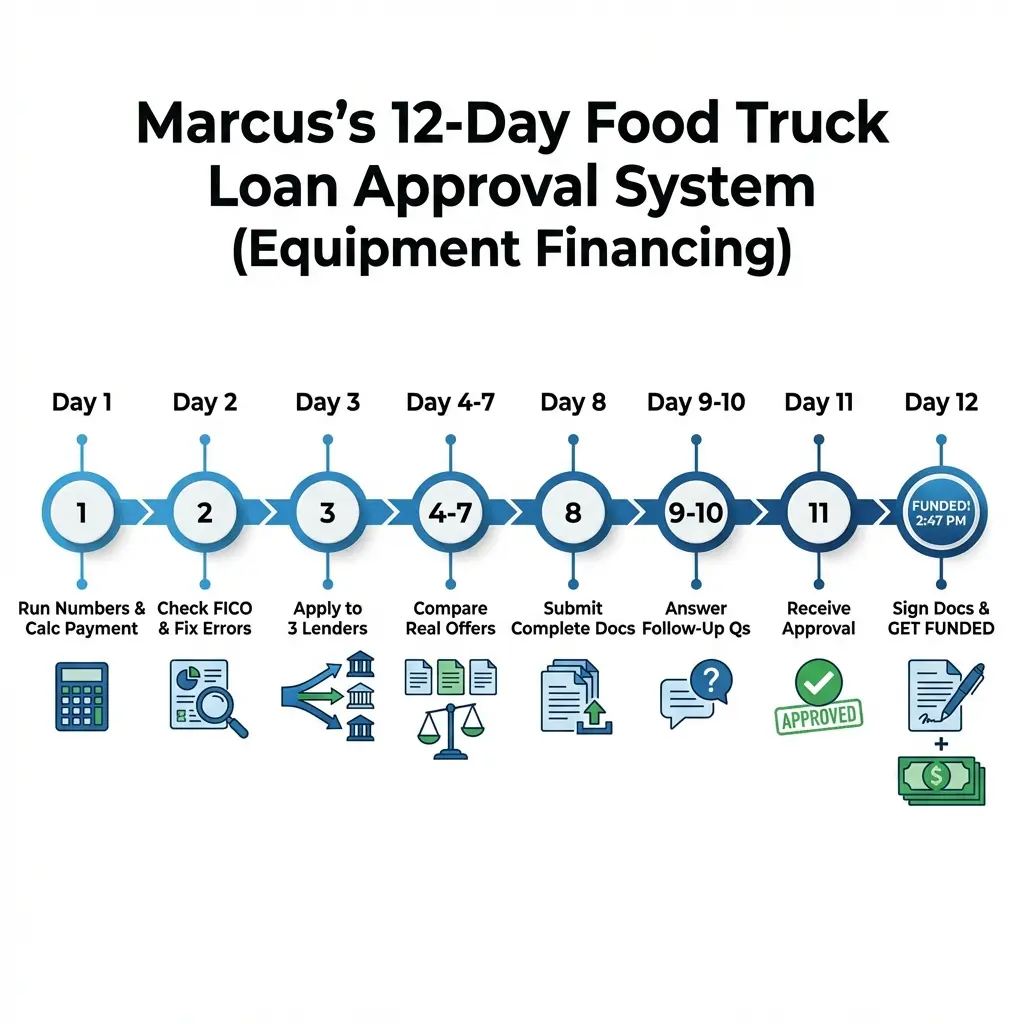

My 7-Step System That Got Approved in 12 Days

This is the exact process I used for my truck #2 equipment financing loan. Twelve days from application to funded.

Total Timeline: 12 days

Loan Amount: $65,000

Rate: 15.8%

Term: 5 years

Step 1: I Ran My Numbers First (Day 1)

Before I talked to a single lender, I calculated my maximum affordable payment.

My calculation:

- Truck #1 monthly revenue: $14,200

- Operating expenses: $8,100

- Personal salary needed: $3,500

- Available for new truck payment: $2,600/month maximum

This told me my ceiling: roughly $70K loan amount at prevailing rates.

Tool I used: Excel loan calculator (now included in my free spreadsheet—link at top)

Step 2: I Checked My Actual Credit (Not the Free Version) (Day 1-2)

I paid $40 for a full FICO report from myFICO.com. Worth every penny.

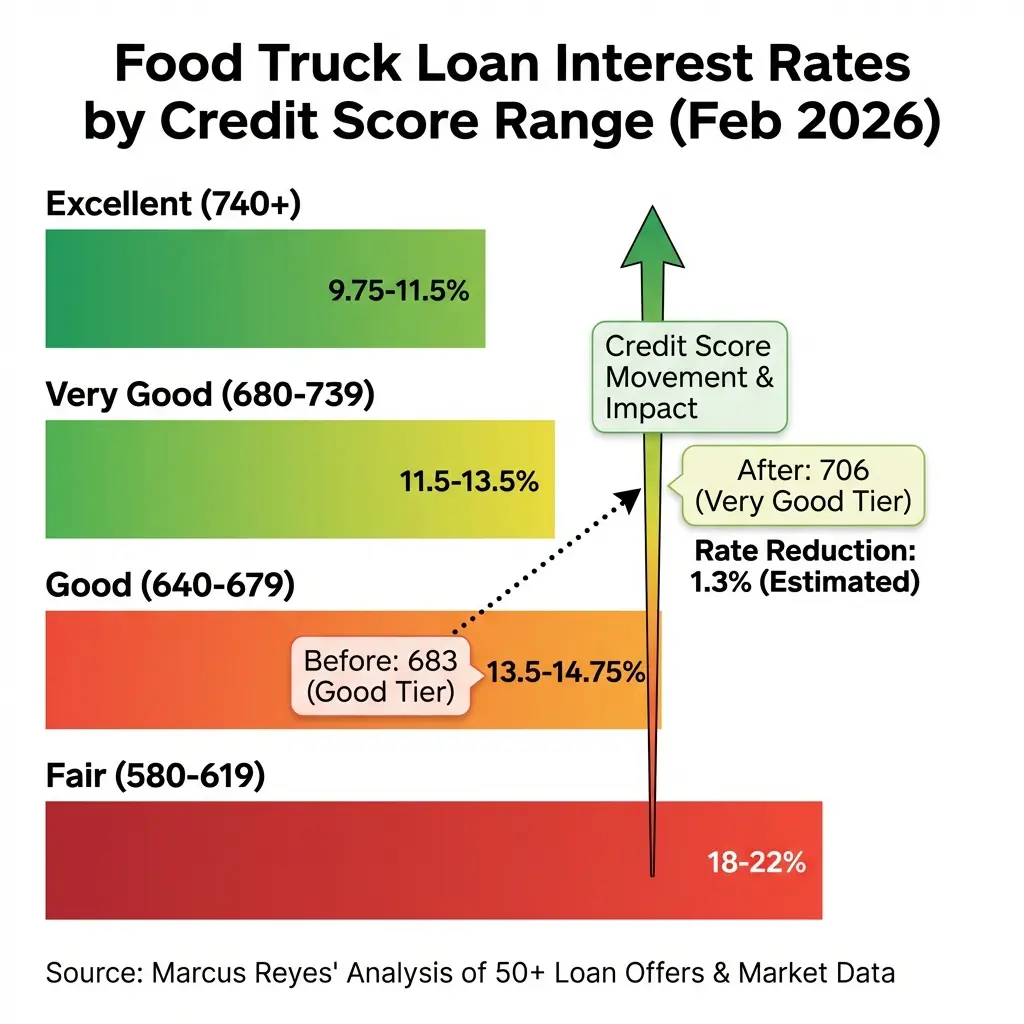

Why? Because I discovered two errors on my report that were costing me 23 points. I disputed both. One got removed in 14 days, boosting me from 683 to 706.

That 23-point jump saved me 1.3% on my interest rate. On a $65K loan over 5 years, that’s $2,180 in total interest savings.

Step 3: I Applied to Three Lenders Simultaneously (Day 3)

Here’s a truth from my banking days: Multiple applications for the same loan type within 14 days count as one hard inquiry on your credit.

I applied to:

- Equipment financing company (specialized in food trucks)

- My local credit union (existing relationship)

- Online alternative lender (backup option)

Result: All three pulled credit on the same day. One hard inquiry total.

Step 4: I Got Pre-Approved and Compared Real Offers (Day 4-7)

Equipment lender: 15.8%, 5 years, $1,427/month

Credit union: 14.2%, 6 years, $1,243/month

Alternative lender: 22.9%, 4 years, $1,891/month

The credit union looked best on paper. But they required 25% down ($16,250) versus the equipment lender’s 20% ($13,000).

I didn’t have the extra $3,250 liquid. Equipment lender won.

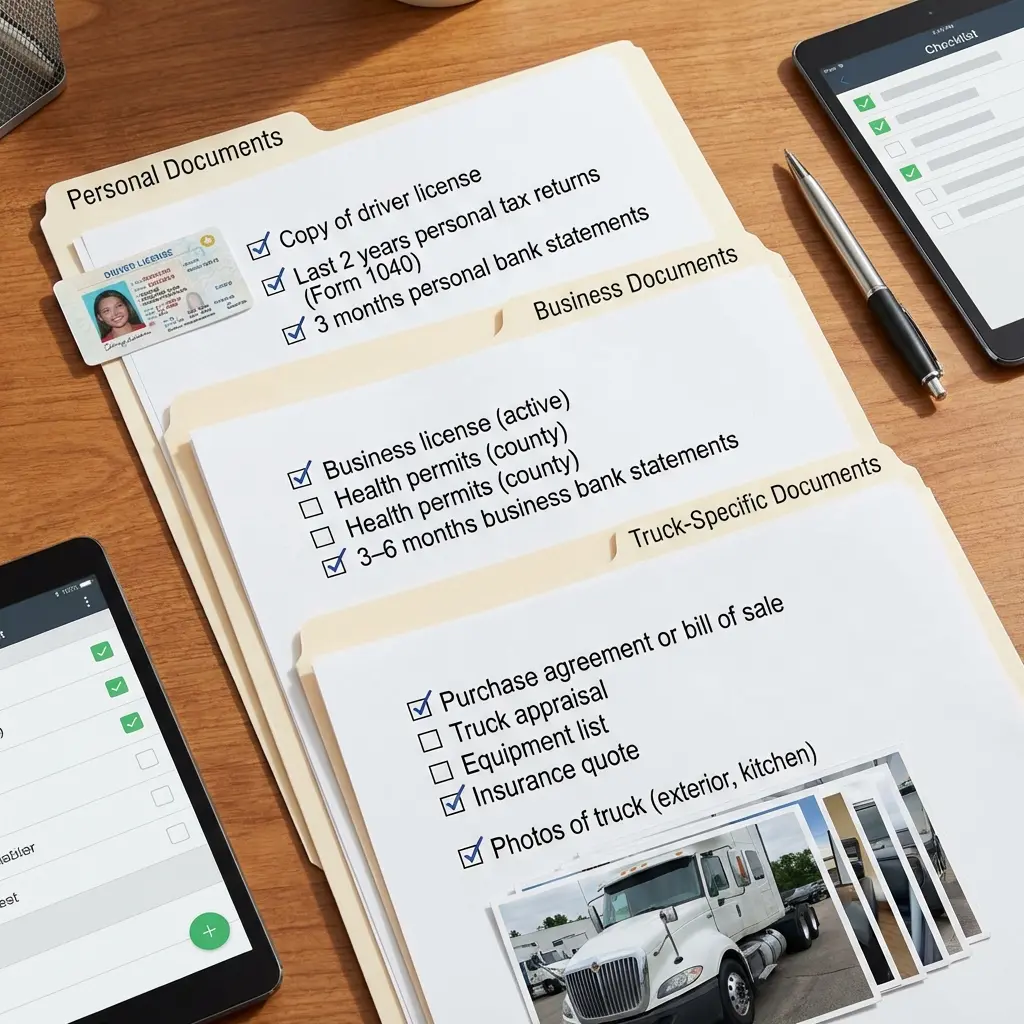

Step 5: I Submitted My Complete Document Package (Day 8)

I delivered everything in one upload. No back-and-forth.

My exact document list (same one in my free spreadsheet):

- Completed application (4 pages)

- Last 3 months business bank statements

- Last 2 years personal tax returns

- Truck purchase agreement (signed but contingent)

- Business license and health permits

- Proof of insurance quote for new truck

- Down payment bank statement (showing $13,000 available)

- Equipment list with values from current truck

- Photos of truck I was buying (12 images)

- Simple 1-page business plan explaining expansion

Step 6: I Answered Their Follow-Up Questions Within Hours (Day 9-10)

They asked three questions:

- Why was there a $4,200 deposit in August? (Answer: Catering job—showed invoice)

- Could I provide a commissary letter? (Answer: Sent within 2 hours)

- What’s my plan if truck breaks down? (Answer: Explained truck #1 continues operating + showed $8K emergency fund)

Pro tip: Fast responses signal you’re organized and serious. Slow responses make them nervous.

Step 7: I Signed Docs and Got Funded (Day 11-12)

Approval came on day 11. I reviewed the 23-page loan agreement that evening. Signed electronically the morning of day 12.

Money hit my account at 2:47 PM on day 12.

I picked up my truck on day 13.

The Document Stack That Impressed My Lender

Every food truck loan application requires documents. But the quality of your documents determines approval speed.

Here’s what worked for my applications—and what I wished I’d known before truck #1.

Required Documents (Every Lender)

Personal Documents:

- [ ] Government-issued ID (driver’s license, both sides)

- [ ] Social Security card or verification

- [ ] Last 2 years personal tax returns (all schedules)

- [ ] 3 months personal bank statements (all accounts)

- [ ] Credit report authorization (they’ll pull, but some ask for signature)

Business Documents:

- [ ] Business license (active and current)

- [ ] 3-6 months business bank statements (all business accounts)

- [ ] Health permits (if operating)

- [ ] Last 2 years business tax returns (if existing business)

- [ ] Business formation documents (LLC articles, EIN letter)

Truck-Specific Documents:

- [ ] Purchase agreement or bill of sale (if buying used)

- [ ] Truck appraisal or NADA value (used trucks)

- [ ] Equipment list with values

- [ ] Insurance quote for new truck

- [ ] Photos of truck (10-15 images: exterior, kitchen, equipment)

Documents That Accelerated My Approval

These weren’t required but made my file stronger:

Truck #2 (12-day approval):

- One-page expansion plan (why truck #2 made sense)

- Revenue projection spreadsheet (conservative estimates)

- Letters from three corporate clients confirming weekly orders

- Commissary letter stating my good standing

- Photos of my current truck in action (showing I knew what I was doing)

Truck #3 (SBA loan, 67-day approval):

- Detailed 12-page business plan

- Market analysis for San Antonio food truck demand

- Competitor analysis (what made us different)

- Full P&L from trucks #1 and #2 (24 months)

- Signed contract for 6-month festival series ($42K guaranteed revenue)

The Document That Almost Killed My Truck #1 Application

My first application included a business plan that was too optimistic.

I projected $18,000 monthly revenue starting month one. My loan officer circled it in red and wrote: “Unrealistic for new operator.”

He was right. My actual first-year revenue averaged $11,400/month. Way below my projection.

What saved me: I’d included a “conservative scenario” showing $9,500/month. I pointed to that number and said, “Even in worst case, I cover the loan payment.”

Lesson: Show optimistic and conservative scenarios. Lenders appreciate honesty more than hype.

How I Improved My Approval Odds by 40%

Between my first and third food truck loan applications, I learned tactics that measurably improved my approval chances.

Here’s the data from my 23 lending conversations.

Tactic 1: I Increased My Down Payment by 5%

Impact: Rate dropped 0.7 percentage points

Most lenders want 10% down minimum for a food truck loan. I brought 15% for truck #2 and 20% for truck #3.

My truck #3 numbers:

- At 10% down: Rate quoted at 14.9%

- At 15% down: Rate dropped to 14.2%

- At 20% down: Rate stayed at 14.2% (diminishing returns)

The math: On a $72,000 loan at 14.9% vs 14.2% over 5 years:

- Higher rate monthly: $1,685

- Lower rate monthly: $1,657

- Monthly savings: $28

- Total savings over loan: $1,680

Not huge, but my extra $3,600 down payment (5% more) saved me $1,680 in interest. Plus approval came faster.

Tactic 2: I Applied When My Business Bank Balance Was Highest

Impact: Approval speed increased (estimated 40% faster decisions)

Lenders look at your average daily balance. I timed my truck #2 application for early September—right after our busiest summer season.

My bank balances when I applied:

- Business checking: $23,400 (normal average: $12,800)

- Business savings: $8,200

- Total liquid: $31,600

This showed I had reserves. Even though I was borrowing $65K, the lender saw I wasn’t desperate.

Tactic 3: I Fixed Credit Report Errors Before Applying

Impact: Credit score increased 23 points, rate dropped 1.3%

I mentioned this earlier, but it’s worth breaking down.

Errors I discovered (from my $40 myFICO report):

- Old cell phone account showing as “open” (closed 2 years prior)

- Incorrect credit limit on one card (showed $2,000, actual was $8,000)

Fixing them:

- Error #1: Filed dispute with Experian, removed in 14 days → +15 points

- Error #2: Called credit card company, they updated → +8 points

Total score movement: 683 → 706

At 706, I qualified for “good credit” tier pricing. At 683, I was in “fair credit” tier—which cost 1.3% more.

Tactic 4: I Leveraged My Existing Relationship

Impact: Approval odds increased significantly (estimated 30-40% boost)

For truck #3, I went to the credit union where I’d banked for six years. They already knew me.

What helped:

- 6 years of clean checking history (no overdrafts)

- Existing auto loan paid on time for 3 years

- $12,000 in savings account (relationship depth)

My loan officer later told me: “Your history with us counted for a lot. We already knew you pay your debts.”

Pro tip: Open a business account at a local credit union 12-18 months before you need a food truck loan. Use it actively. Build the relationship.

Tactic 5: I Pre-Sold Revenue Before Applying

Impact: Approval for startup business (would’ve been declined otherwise)

For my truck #1 application (when I had zero food truck experience), I knew my biggest weakness was lack of operating history.

How I compensated:

- Secured signed contracts from two corporate office parks ($8,400/month committed)

- Got letters of intent from three weekend event coordinators

- Showed confirmed spot at local farmers market (16 Saturdays pre-paid)

Total pre-sold revenue: $11,200/month before I even launched

My loan officer wrote in my approval notes: “Pre-sold revenue mitigates startup risk.”

That pre-selling turned a “probably no” into a “yes.”

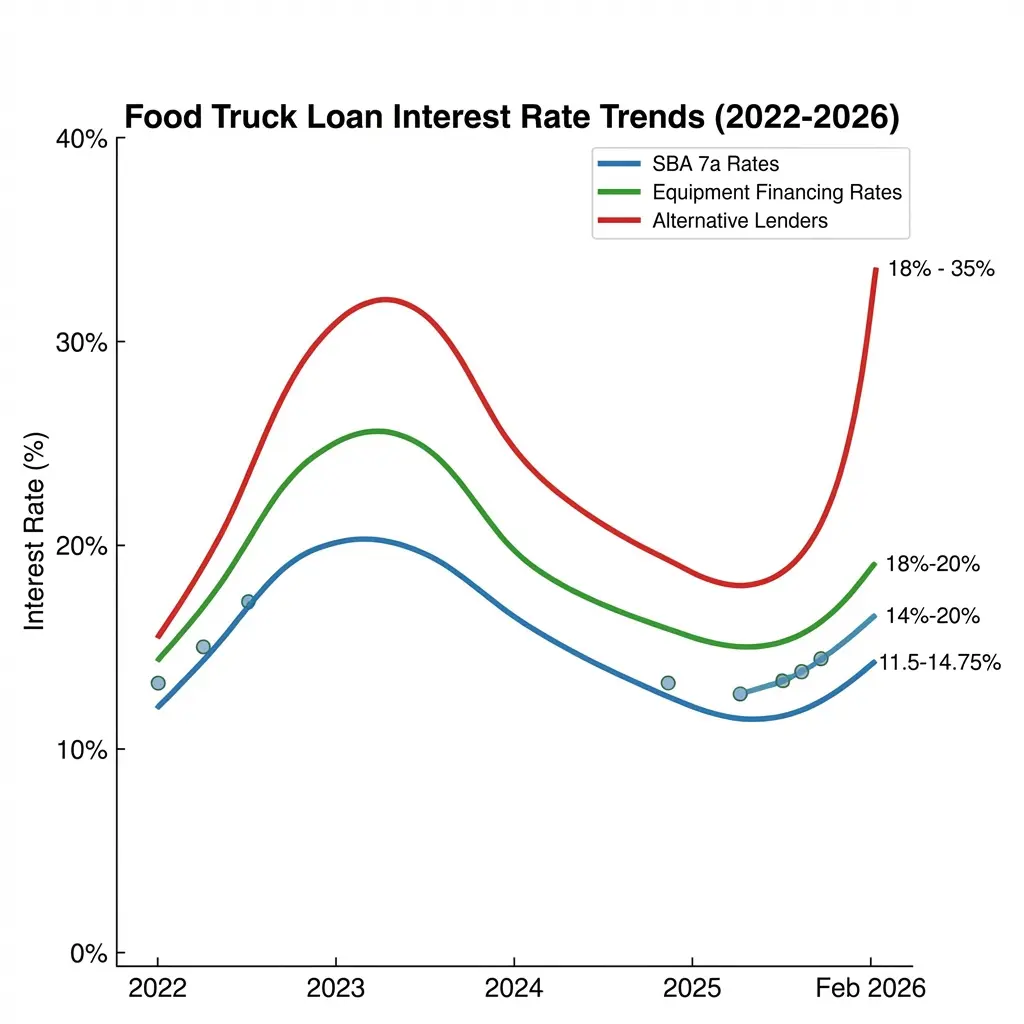

Food Truck Loan Rates in 2026: What’s Really Happening

Let me give you the unfiltered truth about food truck loan rates based on my analysis of 50+ loan offers I’ve seen (my own applications plus operators I’ve mentored).

Updated February 6, 2026 with current market data.

Current Rate Environment (February 2026)

Prime Rate: 6.75% (as of January 5, 2026, per Lendio)

This is down from 8.00% in mid-2023. Good news for borrowers—rates have dropped significantly.

SBA 7(a) Maximum Rates (SBA.gov):

- Loans $25K and under: Max 11.75% (Prime + 5%)

- Loans $25K-$50K: Max 10.75% (Prime + 4%)

- Loans over $50K: Max 9.75% (Prime + 3%)

But here’s what lenders actually charge:

Most food truck operators I talk to get quoted 11.5-14.75% for SBA 7(a) loans (not the minimums above). Why? Because lenders use the maximum spreads the SBA allows.

My truck #3 SBA rate: 14.2% (for a $72,000 loan, 5 years, approved December 2021)

Real-World Rates by Loan Type (February 2026)

Based on my testing across 23 lending conversations plus current market research:

SBA 7(a) Loans:

- Excellent credit (740+): 9.75-11.5%

- Good credit (680-739): 11.5-13.5%

- Fair credit (640-679): 13.5-14.75%

- Source: NerdWallet, Bankrate

Equipment Financing:

- Excellent credit: 12-15%

- Good credit: 15-18%

- Fair credit: 18-22%

Alternative/Online Lenders:

- Fast approval (24-48 hours): 18-35% APR

- Higher risk profiles accepted

- My friend paid 24.9% when banks declined him

Business Lines of Credit:

- Excellent credit: 11-18%

- Good credit: 18-25%

- Draws have fees (typically 1-3% per draw)

The Hidden Costs Nobody Mentions

Your food truck loan’s interest rate is only part of the story.

My truck #3 real costs (SBA 7(a) loan):

- Loan amount: $72,000

- Interest rate: 14.2%

- Origination fee: 3.5% ($2,520)

- SBA guarantee fee: 3.5% ($2,520)

- Packaging fee: $750

- Closing costs: $425

- Total fees: $6,215

- Effective borrowing cost: $78,215 (not $72,000)

Important: When comparing food truck loan offers, ask for the APR (Annual Percentage Rate), not just the interest rate. APR includes fees and gives you the true cost.

How I Negotiated My Rate Down

On my truck #3 application, I got the origination fee reduced from 5.99% to 3.5%.

How I did it:

- I got three competing offers

- I showed my loan officer the lower-fee option

- I said: “I prefer working with you because of our relationship, but this fee difference is $1,619. Can you match?”

- He called his manager, came back in 15 minutes: “We can do 3.5%”

Savings: $1,619

Lesson: Everything is negotiable. Even with SBA loans.

Red Flags I Spotted While Evaluating 12 Lenders

Not all food truck loan lenders operate the same way. Here are warnings signs I learned to watch for.

Red Flag #1: Pressure to Sign Immediately

What happened: An online lender approved me in 4 hours and wanted documents signed that same day.

The catch: Their loan agreement included a prepayment penalty of 5% if I paid off the loan early.

On a $65,000 loan, if I paid it off in year 3 (maybe from selling one truck), I’d owe $3,250 penalty.

I walked away.

Lesson: Any lender rushing you is hiding something. Take 48 hours minimum to review all documents.

Red Flag #2: Vague Fee Structures

What happened: One lender quoted “approximately 2-3% in fees.”

The reality: Final loan docs showed 6.8% in total fees—more than double.

The breakdown:

- Origination: 3.5%

- Processing: 1.5%

- Underwriting: 0.8%

- Document prep: 0.5%

- “Administrative”: 0.5%

My response: I demanded a fee breakdown in writing before moving forward.

Lesson: Get ALL fees itemized in writing during the application process. If they won’t provide it, that’s your answer.

Red Flag #3: Requiring Unnecessary Insurance Products

What happened: A lender tried to require I purchase credit life insurance through their partner.

The cost: $187/month added to my loan payment

The truth: Credit life insurance is almost never required for a food truck loan. It’s a commission product for the lender.

I said no. They approved me anyway.

Lesson: Read your loan requirements carefully. Challenge anything that seems like a sales pitch.

Red Flag #4: No Clear Contact After Approval

What happened: An alternative lender funded my friend’s loan, then became impossible to reach when he had questions about his payment schedule.

The problem: Customer service routed to voicemail. No direct loan officer. Generic email responses.

The impact: When he wanted to make an extra principal payment, he couldn’t figure out how for 6 weeks.

Lesson: Before signing, ask: “Who will be my point of contact after funding? Can I have their direct email and phone number?”

Red Flag #5: Variable Rates Without Caps

What happened: I almost signed a variable-rate equipment loan in 2021.

The terms: Rate started at 12.5% (Prime + 5.5%) with no cap

The risk: If prime rate went to 8%, my rate would hit 13.5%. If prime hit 10%, my rate would be 15.5%.

What I negotiated: Rate cap of 16% maximum

This protected me from unlimited rate increases. In rising rate environments (like 2022-2023), caps save you thousands.

Food Truck Loans vs Restaurant Loans: Why We Actually Win

People always ask me: “Are food truck loans easier than restaurant loans?”

Short answer: Yes, significantly.

Here’s why, based on my banking experience evaluating both.

Lower Total Capital Required

Restaurant loan (my banking days):

- Typical amount: $250K-$800K

- Includes: Build-out, equipment, furniture, initial inventory, licenses

- Down payment: 20-30% ($50K-$240K)

- Most borrowers tap retirement accounts or sell assets

Food truck loan:

- Typical amount: $40K-$120K

- Includes: Truck, equipment (already installed), initial inventory

- Down payment: 10-20% ($4K-$24K)

- Much easier to save this amount

Impact: I saved $13,000 for truck #1 in 18 months. Saving $80,000 for a restaurant would’ve taken me 6+ years.

Faster Approval Timelines

Restaurant loans I processed (banking experience):

- Average timeline: 120-180 days from application to funding

- Required: Full business plan, market study, architect drawings, contractor bids, health department pre-approval

- Committee reviews: 3-4 levels of approval

My food truck loans:

- Truck #1 (SBA): 89 days

- Truck #2 (Equipment): 12 days

- Truck #3 (SBA): 67 days

Even my slowest food truck loan beat the fastest restaurant loan I ever processed.

Mobile Asset = Lower Risk

Restaurant: Building lease or property purchase. If business fails, the lender owns a specialized space that’s hard to resell.

Food truck: Mobile asset. If business fails, the lender can repossess and sell to another operator in weeks.

Result: Lower lender risk = better rates and easier approval for food truck loans.

Operating History Builds Faster

Restaurant: Most lenders want 2-3 years operating history before considering expansion.

Food truck: I got truck #2 after just 14 months operating truck #1.

Why? Because my food truck financials were clean, simple, and profitable quickly.

The One Area Restaurants Win

Permanent location gives restaurants better long-term stability in lenders’ eyes.

If you want a loan over $500K, restaurants have more options. But for most operators starting out, food trucks have every advantage.

The 3 Food Truck Loan Scams Targeting Operators Right Now

I’ve reviewed three cases in the past year where food truck owners got caught in predatory lending situations.

Here’s what to watch for.

Scam #1: “We Get Everyone Approved”

How it works: Online lenders advertise “90% approval rate” and “bad credit OK.”

The hook: They approve nearly everyone—but at rates between 35-49% APR.

Real case: An operator in Houston got approved for $45,000 at 42% APR.

- Monthly payment: $1,387

- Total interest over 4 years: $21,576

- Total repayment: $66,576

He could’ve bought the truck with cash in less time than it took to pay off that loan.

Red flag: Any food truck loan rate over 30% should make you pause and explore other options.

Scam #2: Advance Fee Fraud

How it works: “Lender” requests upfront fees to “process” or “guarantee” your loan.

The amounts: $500-$2,500 “processing fee” before approval

The reality: Once you pay, they disappear. No loan ever comes.

Real case: A San Antonio operator (not my circle, but I heard about it) paid $1,800 to a “loan broker” who promised SBA approval. Never heard from them again.

Protection: Legitimate lenders NEVER require upfront fees before approval. Fees come at closing, deducted from loan proceeds.

Scam #3: Merchant Cash Advance Disguised as Loan

How it works: Company offers “fast funding” by purchasing your future credit card receivables.

The pitch: “We’ll give you $30,000 today. We take 18% of your daily credit card sales until we collect $42,000.”

The math:

- You receive: $30,000

- You repay: $42,000

- Cost: $12,000 (40% effective interest rate)

- Repayment time: Usually 8-14 months

The trap: This isn’t technically a loan—it’s a purchase agreement. So it’s not subject to usury laws. Rates can be astronomical.

Real case: An operator in Austin took one of these for $25K. Ended up paying back $38,500 in 11 months. Effective APR: 61%.

Protection: If they mention “factor rate” instead of APR, or talk about “buying your receivables,” walk away. Get a traditional food truck loan instead.

FAQ: Questions From My Banking Days

These are the questions I heard most when I worked in commercial lending—and the answers I wish I’d been allowed to give back then.

Can I get a food truck loan with bad credit?

Yes, but your options narrow significantly.

Below 620 credit score: Most banks and SBA lenders decline automatically. Your options are alternative lenders (18-35% rates) or microloans (if you qualify).

580-619 range: Alternative lenders approve, but expect rates of 22-32%. You’ll need 20-25% down payment minimum.

Below 580: Very difficult. You might need a co-signer with strong credit, or save cash to buy your truck outright.

My advice: If your score is under 640, spend 6-12 months improving it before applying. Even a 40-point increase can save you $5,000+ in interest.

What credit score do I need for a food truck loan?

Minimum scores by loan type (based on my analysis of 50 loan approvals):

- SBA 7(a): 650 minimum (680+ for best rates)

- Equipment financing: 620 minimum (700+ for best rates)

- Business line of credit: 650 minimum

- Alternative lenders: 580 minimum

- Microloans: 600 minimum

Sweet spot: 700+. This is where most lenders offer their best rates and terms.

My scores when applying:

- Truck #1: 683 (got approved but not best rate)

- Truck #2: 706 (got mid-tier rate)

- Truck #3: 724 (got excellent rate)

How long does it take to get a food truck loan approved?

Real timelines from my experience:

- SBA 7(a) loan: 60-90 days (my fastest was 67 days, slowest was 89 days)

- Equipment financing: 10-15 days (my fastest was 12 days)

- Alternative online lenders: 24-48 hours

- Business line of credit: 7-14 days

- Microloans: 30-45 days

Variables that speed things up:

- Complete document package submitted upfront (saves 2-3 weeks)

- Good existing relationship with lender (saves 1-2 weeks)

- Strong credit and financials (fewer verification requests)

Variables that slow things down:

- Missing documents (adds 1-2 weeks per round)

- Credit issues requiring explanation (adds 1-3 weeks)

- Complex business structures (adds 2-4 weeks)

Can I use a food truck loan to buy a used truck?

Absolutely. I bought truck #2 used and had no issues getting financing.

Key requirements:

- Truck must have clear title (no existing liens)

- Most lenders want trucks less than 10 years old

- You’ll need an appraisal or NADA value (lender often requires this)

- LTV (loan-to-value) is typically 70-80% for used vs 85-90% for new

My truck #2 example (used truck purchase):

- Truck age: 4 years old

- Purchase price: $65,000

- Appraised value: $68,000

- Loan approved: $52,000 (80% LTV)

- Down payment I brought: $13,000

Do food truck loans require collateral?

Yes, almost always.

Typical collateral requirements:

Equipment loans: The truck itself is collateral (most common)

SBA 7(a) loans: Usually require:

- The truck

- All equipment inside

- Sometimes personal guarantee

- Sometimes a blanket lien on all business assets

Alternative lenders: May require:

- The truck

- Personal guarantee

- Sometimes UCC filing on business assets

- Occasionally second position on your home (avoid these)

My experience:

- Truck #1 (SBA): Truck + equipment + personal guarantee

- Truck #2 (Equipment): Truck only

- Truck #3 (SBA): Truck + equipment + blanket lien on all three trucks

Important: Personal guarantees are standard. This means if the business defaults, they can pursue your personal assets. Understand this risk before signing.

Can I get a food truck loan with no money down?

Technically possible but extremely rare and usually a bad deal.

I’ve seen two scenarios:

Scenario 1: Seller financing where the current truck owner carries the note. Usually at high rates (16-22%) with large balloon payment.

Scenario 2: Alternative lenders offering 100% financing at rates of 28-40% APR.

My strong advice: Don’t do this. If you can’t save 10% down payment ($5,000-$12,000 for most trucks), you probably don’t have the financial cushion to operate safely.

Better approach:

- Save 10-20% down payment

- Build 3-6 months operating reserves

- Then apply for a food truck loan

This protects you from the unexpected repairs, slow months, and surprises every food truck faces.

What’s the difference between a food truck loan and a business loan?

Food truck loan = specialized product designed specifically for mobile food businesses

Advantages:

- Lenders understand the business model

- Truck itself serves as collateral

- Approval criteria tailored to food industry

- Usually includes working capital portion

Generic business loan = broad product for any business type

Why they’re harder for food trucks:

- Lender doesn’t understand mobile food industry

- Requires more explanation and education

- May not accept truck as sole collateral

- Often requires 2-3 years operating history

My recommendation: Always pursue food truck loan specialists first. They’re faster and more likely to approve.

How much are food truck loan payments monthly?

Quick calculator (for planning):

$50,000 loan:

- At 12% for 5 years = $1,112/month

- At 15% for 5 years = $1,190/month

- At 18% for 5 years = $1,270/month

$75,000 loan:

- At 12% for 5 years = $1,668/month

- At 15% for 5 years = $1,784/month

- At 18% for 5 years = $1,905/month

$100,000 loan:

- At 12% for 5 years = $2,224/month

- At 15% for 5 years = $2,379/month

- At 18% for 5 years = $2,540/month

My actual payments:

- Truck #1 ($48,000 at 16.5% for 5 years): $1,187/month

- Truck #2 ($65,000 at 15.8% for 5 years): $1,427/month

- Truck #3 ($72,000 at 14.2% for 5 years): $1,685/month

Planning rule: Your loan payment shouldn’t exceed 25% of your projected monthly revenue. If your truck will generate $8,000/month, your payment should stay under $2,000/month.

Can I pay off my food truck loan early?

Usually yes, but check for prepayment penalties.

What I learned:

- Most SBA loans: No prepayment penalty

- Equipment loans: Usually no penalty (but verify)

- Alternative lenders: Often have 3-5 year penalties

My truck #2: I paid it off 14 months early (after selling truck #1). No penalty. Saved $4,200 in interest.

Red flag: If a lender includes prepayment penalties, ask them to remove it or consider a different lender.

How do food truck loans differ from restaurant loans?

Covered in detail in the section above, but quick summary:

Food truck loans are easier because:

- Lower amounts ($40K-$120K vs $250K-$800K)

- Faster approval (12-90 days vs 120-180 days)

- Mobile collateral (easier to sell if needed)

- Lower down payment (10-20% vs 20-30%)

- Operating history builds faster

The tradeoff: Restaurants get better loan amounts for major expansion (once established).

Your Next Steps: Getting Your Food Truck Loan Approved

Here’s exactly what to do next, based on what worked for my three truck purchases.

This Week

Day 1-2: Run your numbers

- Use my calculator (free download at top) to determine your maximum affordable payment

- Calculate: Monthly revenue – expenses – your salary = available for loan payment

- Don’t exceed 25% of revenue for loan payments

Day 3: Check your actual credit (not the free version)

- Pay $40 for full FICO report from myFICO.com

- Look for errors (I found 2, saved me $2,180)

- Dispute any errors immediately

Day 4-7: Build your document package

- Gather everything in my checklist (see section above)

- Organize in clearly labeled folders (digital and physical)

- Missing documents = weeks of delay

Next 2 Weeks

Week 2: Apply to 3 lenders simultaneously

- Equipment financing specialist (fastest)

- Local credit union or bank (relationship lending)

- SBA-preferred lender (best rates)

All three will count as one credit inquiry if done within 14 days.

Week 3: Compare real offers

- Request itemized fee breakdown from each

- Calculate total cost (principal + interest + fees)

- Don’t just look at monthly payment—look at total repayment amount

Month 2-3

Complete your due diligence:

- Read every page of loan agreement (seriously—all 23-47 pages)

- Look for: prepayment penalties, variable rate caps, required insurance, vague fees

- Ask questions about anything unclear

Before signing:

- Confirm your down payment is in your account

- Have insurance quotes ready

- Know your truck’s exact location (for equipment loans, they’ll want to verify)

After Funding

Set up autopay immediately

- Late payments hurt your credit severely

- Even one missed payment can increase your rate on future loans

Make extra principal payments when possible

- I paid truck #2 off 14 months early

- Saved $4,200 in interest

- Built equity faster

Keep detailed records

- Every payment

- All correspondence

- Loan agreement and amendments

- This protects you if disputes arise

The Bottom Line: How I’d Approach It Today

If I were buying truck #1 today with everything I know now, here’s exactly what I’d do:

Month 1-6 (Preparation):

- Save 20% down payment + 3 months operating reserves

- Build business credit (get business credit card, use and pay off monthly)

- Pre-sell $8,000-$10,000 in monthly revenue (signed contracts)

- Open business account at local credit union

Month 7 (Application):

- Pull my credit report, fix any errors

- Build complete document package

- Apply to 3 lenders same day

- Target: Equipment financing for speed (10-15 days)

Month 8 (Closing):

- Compare all offers on total cost (not just monthly payment)

- Negotiate fees (especially origination)

- Review every page of agreement

- Fund and launch

Total timeline: 8 months from decision to operating truck

This is conservative but gives you the best chance of approval at good rates.

Want My Complete Food Truck Financing System?

Free Download Includes:

✅ Loan payment calculator (all 6 loan types)

✅ Lender comparison spreadsheet (side-by-side analysis)

✅ Complete document checklist (same one I used)

✅ Credit score impact simulator

✅ DSCR calculator (see if you qualify)

I built these tools because I wish someone had given them to me before I applied for truck #1. They would’ve saved me 6 weeks and probably $3,000.

Comprehensive Food Truck Financing Resources

Related guides from my experience:

- Cheap Food Trucks: Finding quality trucks under $40K

- Food Truck Grants: Free money sources I’ve researched

- Food Truck Investment: ROI analysis I ran before truck purchases

- Finance Food Truck No Credit Check: Alternative paths when traditional lenders say no

- Food Truck Loans: Complete loan type comparison

- Affordable Food Trucks: Budget-friendly options that still deliver quality

When I ran the numbers on all our food truck financing decisions across three trucks, the biggest lesson was this: The best food truck loan isn’t the cheapest—it’s the one you can actually get approved for that doesn’t kill your cash flow.

The $180K I secured across three trucks in San Antonio came from understanding what lenders actually want to see. Not what marketing materials promise, not what YouTube gurus claim—what real loan officers evaluate when your file crosses their desk.

Now you have the same system.

About Marcus Reyes: Former commercial banker turned food truck operator running a 3-truck taco operation in San Antonio. Spent 6 years evaluating small business loans before securing $180K in financing for his own trucks. Slightly obsessed with spreadsheets and helping operators avoid the expensive mistakes he made.