With food truck loan rates ranging from 5% to 36% APR and approval timelines spanning 2 days to 90 days depending on the lender, which financing path actually fits your business?

Quick answer: The right loan type depends on your credit profile, how much you need, and how fast you need it. Food truck loans typically range from $5,000 to $200,000, with equipment financing offering the lowest rates for truck purchases and SBA loans providing the best long-term terms for established operators. Most food truck owners overpay on interest simply because they don’t compare loan types systematically.

When I helped finance our second and third trucks, I evaluated over a dozen lending options. That process — and my years in commercial banking before it — taught me that the financing structure matters as much as the truck itself.

📚 Part of our complete Food Truck Financing guide.

Disclaimer: This article is for informational purposes only and does not constitute professional financial advice. Rates, terms, and requirements change frequently. Consult a qualified financial advisor or lender before making borrowing decisions.

What is a food truck loan? A food truck loan is a type of business financing used to purchase, build, or equip a mobile food service vehicle. These loans can come from banks, credit unions, online lenders, nonprofit organizations, or government-backed programs like the SBA. The vehicle or equipment often serves as collateral, which typically results in more favorable rates than unsecured business loans.

The True Cost of Financing a Food Truck

The total cost of launching a food truck extends well beyond the vehicle’s sticker price, and understanding the full number is the first step toward choosing the right loan amount and type.

A new, custom-built food truck typically costs between $50,000 and $200,000 depending on size, kitchen configuration, and equipment specifications — with premium custom builds reaching $300,000 or more. Used food trucks generally fall in the $30,000 to $100,000 range, though they may require additional investment for equipment upgrades or cosmetic repairs. A basic food trailer — a more affordable entry point — can run $15,000 to $50,000.

The truck itself is only part of the equation. When I built out our financial model for the second truck, the vehicle represented roughly 60% of total startup costs. The remaining 40% covered permits, initial inventory, insurance deposits, wrap design, POS hardware, and a working capital cushion for the first few months of operations. For a $100,000 truck, that means you’re realistically looking at $140,000 to $165,000 in total capital needs.

This distinction matters for financing because some loan types — specifically equipment loans — only cover the vehicle and kitchen equipment. You’ll need separate financing or savings for everything else. Understanding the full picture prevents the common mistake of securing a truck loan and then running out of cash before your first event.

If you’re still estimating your total investment, our food truck cost breakdown walks through every line item.

Food Truck Loan Types Compared

Food truck business loans come in six primary types, each suited to different business stages and financial profiles. Here’s how they compare side by side.

| Loan Type | Typical Amount | APR Range | Term | Min. Credit Score | Best For |

|---|---|---|---|---|---|

| SBA 7(a) Loan | $5,000–$5 million | 11%–16% | Up to 10 years (equipment) | 680+ | Established businesses seeking best rates |

| SBA Microloan | Up to $50,000 | 8%–13% | Up to 6 years | 620+ | Startups needing smaller amounts |

| Equipment Financing | $10,000–$500,000 | 5%–36% | 1–7 years | 600+ | Buying the truck or major kitchen equipment |

| Business Term Loan | $5,000–$500,000 | 7%–30% | 1–5 years | 600–680+ | General business funding, flexible use |

| Business Line of Credit | $5,000–$250,000 | 8%–60% | Revolving | 600+ | Working capital, inventory, emergencies |

| Microloan (Non-SBA) | $500–$50,000 | 8%–22% | Up to 6 years | No minimum (some lenders) | Startups, bad credit, underserved communities |

Rates shown are approximate ranges compiled from multiple lender sources including SBA.gov and individual lender websites as of early 2026. Your actual rate will depend on your qualifications, loan size, and lender. Verify current rates directly before applying.

This table summarizes the main food truck financing options available today. Here’s how to read it: if you’re buying a truck with decent credit and at least a year of food industry experience, equipment financing is typically your most cost-effective path. The truck itself serves as collateral, which reduces lender risk and on average translates to lower rates than unsecured alternatives. If you need broader funding — truck plus working capital plus initial inventory — an SBA 7(a) loan offers the best terms, but the application process takes significantly longer.

When I ran the numbers on our fleet expansion, equipment financing at roughly 10% over 5 years beat the business term loan option by several thousand dollars in total interest. The tradeoff was flexibility: the equipment loan only covered the truck, while a term loan would have funded everything in one package. It’s worth considering that the cheapest loan on paper isn’t always the best fit if it leaves you short on operating capital.

The Bottom Line: For most food truck purchases, equipment financing delivers the lowest total cost of borrowing. SBA loans beat it on rate but take 30–90 days to close. Business term loans cost more but fund faster and cover more expenses. Match the loan type to your specific timeline and capital need — not just the interest rate.

For a deeper look at specific lender options, check our food truck loan comparison.

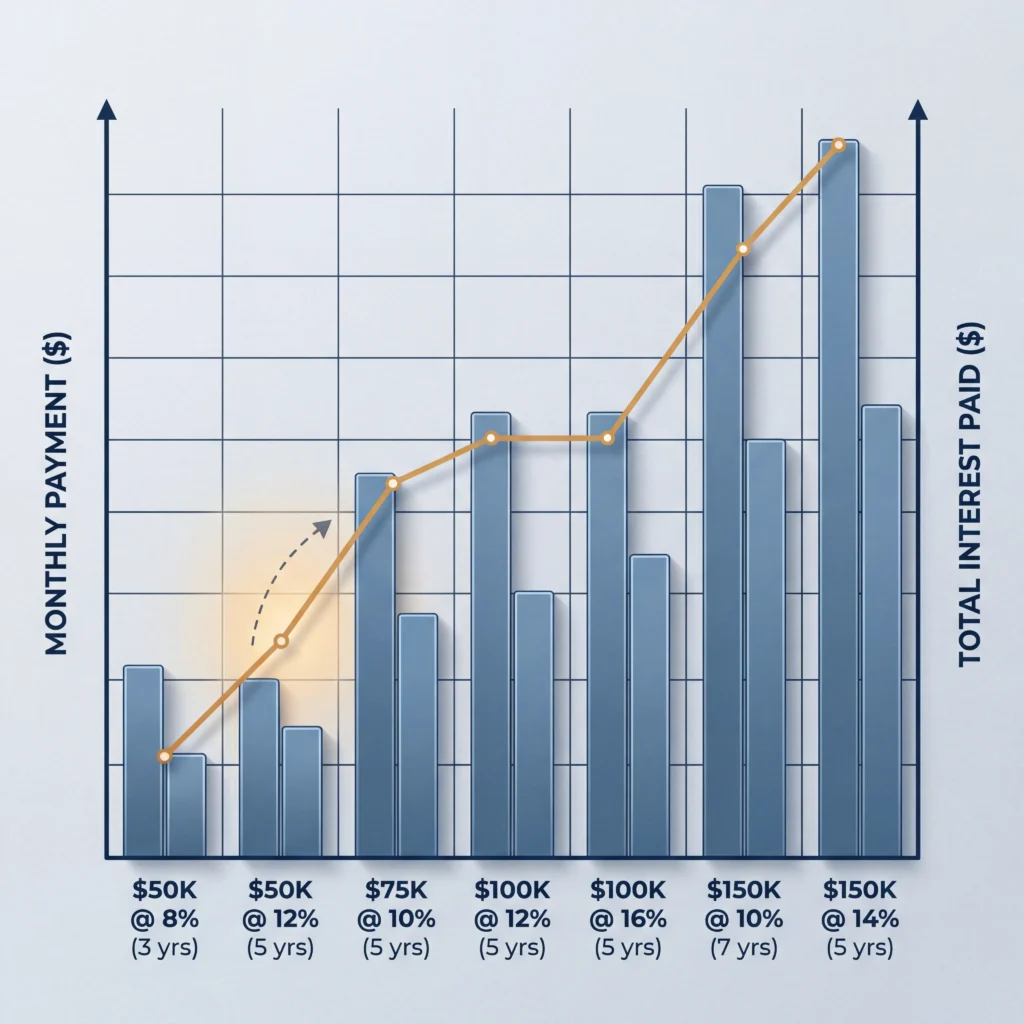

Current Interest Rates and Monthly Payment Breakdown

Your monthly payment on a food truck loan depends on three variables: the amount borrowed, the interest rate, and the repayment term. Here’s a realistic breakdown based on standard amortization across common loan scenarios.

| Loan Amount | APR | Term | Monthly Payment | Total Interest Paid |

|---|---|---|---|---|

| $50,000 | 8% | 3 years | ~$1,567 | ~$6,400 |

| $50,000 | 12% | 5 years | ~$1,112 | ~$16,750 |

| $75,000 | 10% | 5 years | ~$1,593 | ~$20,600 |

| $100,000 | 12% | 5 years | ~$2,224 | ~$33,450 |

| $100,000 | 16% | 5 years | ~$2,431 | ~$45,900 |

| $150,000 | 10% | 7 years | ~$2,494 | ~$59,500 |

| $150,000 | 14% | 5 years | ~$3,492 | ~$59,550 |

Calculated using standard amortization. Rates as of early 2026 — verify with lenders before committing.

These figures illustrate a critical principle: extending the term from 3 to 5 years drops your monthly payment substantially, but can more than double total interest paid over the life of the loan. A food truck loan calculator can help you test different scenarios, but the benchmarks above give you a working framework before you ever talk to a lender.

Real-World Scenario: Say you’re buying a $100,000 custom truck. You put 20% down ($20,000) and finance $80,000 through an equipment loan at 12% APR over 5 years. Your monthly payment comes to roughly $1,779. Over 60 months, you’ll repay approximately $106,760 total — meaning $26,760 goes to interest. Add a typical 2%–5% origination fee ($1,600–$4,000) and your true cost of financing lands between $28,360 and $30,760. That’s the number most operators never calculate until it’s too late.

Based on my experience running three trucks, here’s how I think about it: your monthly food truck loan payment should stay below roughly 15% to 20% of your projected monthly gross revenue. If you’re projecting $15,000 per month in revenue — achievable for a well-located truck with strong foot traffic — your payment should stay under approximately $2,250 to $3,000. Anything beyond that compresses margins to a point where one slow week becomes a crisis.

The Bottom Line: Don’t just compare monthly payments — compare total cost of borrowing. A lower monthly payment with a longer term often costs thousands more in total interest. Run the full amortization before signing anything.

Looking at the data from these payment scenarios, the next question is obvious: which government-backed programs offer the best deal — and what changed recently?

SBA Loans for Food Trucks: What Changed in 2025–2026

SBA loans remain the most favorable financing option for qualified food truck operators, offering longer terms and lower interest rates than most alternatives — but the rules tightened significantly in 2025, and those changes are still in effect.

⚠️ Note: SBA citizenship, residency, and collateral requirements are evolving rapidly. The information below reflects rules as of February 2026. Check SBA.gov for the latest requirements before applying.

The SBA 7(a) program provides terms up to 10 years for equipment purchases, with rates tied to the prime rate plus a spread — currently landing in the 11% to 16% range depending on loan size and term. For food truck purchases classified as equipment, this remains the gold standard in business lending.

Here’s what changed: as of March 27, 2025, the SBA reinstated upfront guaranty fees and lender service fees that had been temporarily reduced. For most borrowers, this means additional closing costs that weren’t a factor in prior years. Additionally, new collateral requirements took effect — the threshold for requiring collateral dropped from $500,000 to $50,000. Since most food truck loans exceed $50,000, nearly every applicant now needs to pledge collateral.

When these changes took effect, I recalculated projected borrowing costs for a potential fourth truck. The reinstated fees alone added over $2,000 to the projected closing costs on a $100,000 loan — a line item that simply didn’t exist the year before.

There’s also a December 2025 update: the SBA now requires 100% of business owners to be U.S. citizens or nationals with a principal residence in the United States. This requirement is still being refined and may tighten further, so verify current eligibility directly with the SBA or your lender.

The data suggests that SBA loans still offer the best rates, but the total cost of borrowing went up, the paperwork got heavier, and the collateral bar got lower. If you’re a startup without assets to pledge, SBA microloans (up to $50,000, with more flexible collateral rules) may now be a more realistic entry point than the standard 7(a) program.

For information on building your case for SBA approval, see our guide to food truck business plans.

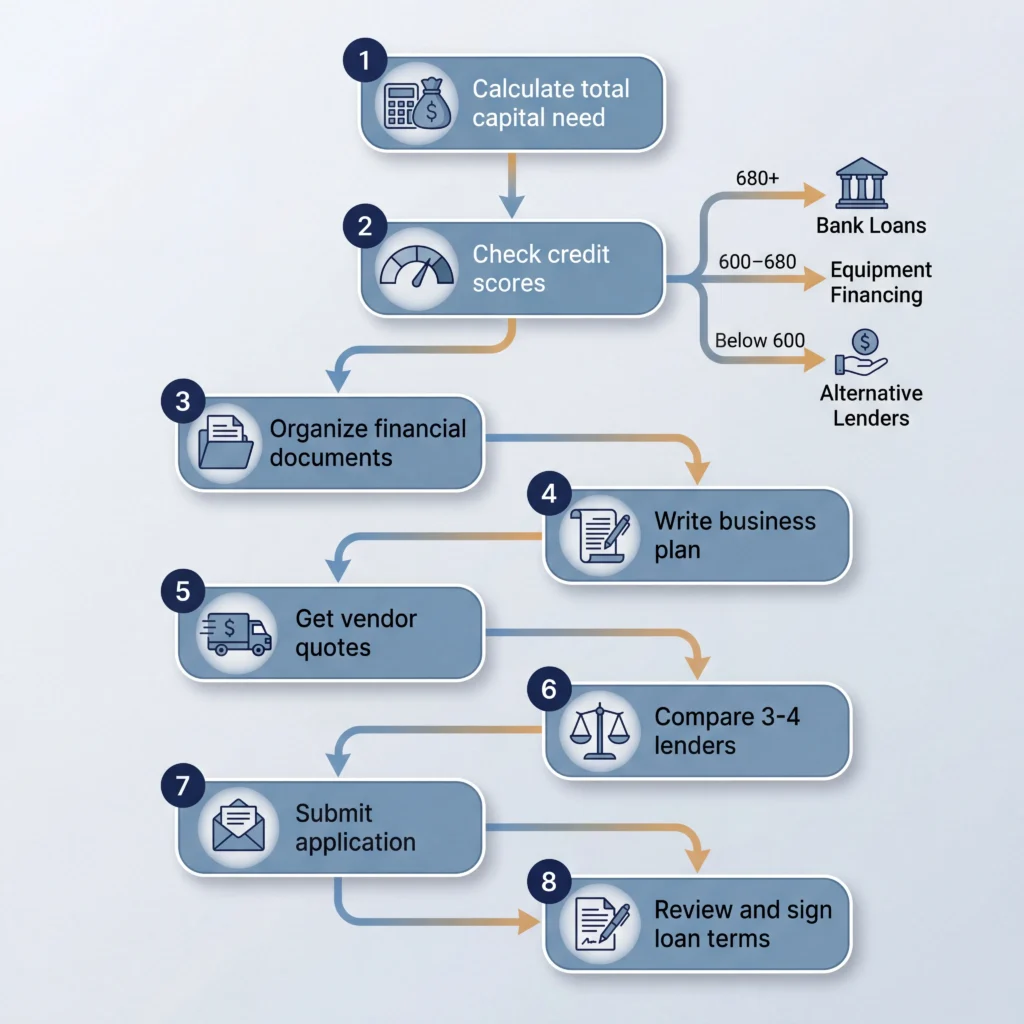

The 8-Step Process for Securing a Food Truck Loan

Securing a food truck loan is harder than applying for a car loan but more straightforward than most commercial real estate financing. Here’s the process I recommend based on both my banking background and my own experience as a borrower, broken down into steps that specifically address where most applicants go wrong.

Step 1: Determine your total capital need. Don’t just price the truck. Add equipment, permits, insurance, initial inventory, wrap and branding, and 3 months of operating capital. When we modeled our second truck’s costs, the non-vehicle overhead accounted for roughly 40% of the total budget — a gap that would have left us short if we’d only financed the truck itself. Round up by 10% for unexpected costs.

Step 2: Check your credit scores — both personal and business. Most food truck lenders look at personal credit, specifically for startups. A score above 680 opens the widest range of options. Between 600 and 680, you’re looking at equipment financing or microloans. Below 600, you’ll need alternative paths covered later in this guide.

Step 3: Organize your financial documents. At minimum: 2 years of personal tax returns, bank statements covering 3–6 months, a personal financial statement, and your business plan with revenue projections. If your business is already operating, add business tax returns and a profit and loss statement. Missing a single document is one of the most common reasons I’ve seen applications stall in the review queue.

Step 4: Write a business plan with realistic projections. Lenders aren’t looking for optimistic fantasies — they want to see that you understand your costs, your market, and your break-even timeline. I’ve seen applications rejected not because the numbers were bad, but because the projections weren’t credible. Conservative, well-researched projections built on documented market data outperform optimistic guesses every time.

Step 5: Get a vendor quote for the truck. Equipment lenders and SBA lenders both require a formal quote from the seller or builder. Shopping at least 2–3 vendors and getting quotes in writing not only satisfies the lender’s requirement but also gives you negotiating leverage and a realistic price benchmark. Some food truck manufacturers work directly with financing partners, which can streamline the process.

Step 6: Compare at least 3–4 lenders. Don’t take the first offer — when we compare across the industry, even a half-point difference in APR on a $100,000 loan translates to over $1,500 in savings over 5 years. Compare APR (not just the interest rate — APR includes fees), repayment terms, funding speed, prepayment penalties, and down payment requirements.

Step 7: Submit your application. Double-check that all documents are current, all fields are completed, and your business plan matches your financial projections. Inconsistencies between your revenue forecast and your bank statements are a red flag that slows processing and raises doubts about your preparation.

Step 8: Review loan terms carefully before signing. Look beyond the monthly payment — specifically examine the total cost of the loan, any balloon payments, personal guarantee requirements, and what happens if you default. If anything is unclear, ask. As a former banker, I can tell you: lenders expect questions, and borrowers who don’t ask any make lenders more nervous, not less.

For a full walkthrough of food truck startup costs that feeds into Step 1, see our food truck startup costs guide.

Food Truck Financing with Bad Credit: Real Options That Work

Getting a food truck loan with bad credit is harder — but the data from nonprofit and alternative lenders shows that viable paths exist for borrowers with scores well below 650, as long as you know where to apply and what tradeoffs to expect.

If your credit score falls below 650, traditional bank loans and SBA 7(a) loans are likely off the table. Several operators I’ve mentored started with scores in the low 600s, and while the process was slower and the rates were higher, every one of them secured financing within 90 days by targeting the right lender type.

Community Development Financial Institutions (CDFIs) are nonprofit lenders specifically designed to serve borrowers that banks overlook. Organizations like Accion Opportunity Fund offer food truck loans from $5,000 to $200,000 with minimum FICO scores as low as 600 — and some CDFIs accept borrowers with no FICO score at all. Rates are higher than SBA loans (typically 14%–17% for food truck specifically), but these lenders also provide business coaching and support that traditional lenders don’t offer.

Equipment financing with a larger down payment is another path. Because the truck serves as collateral, some equipment lenders will approve borrowers with scores in the 550–620 range if you put down 20% to 30%. The math is straightforward: more skin in the game reduces lender risk, and the ROI on that larger down payment shows up as lower monthly obligations and reduced total interest.

Microloans from nonprofit organizations focus on underserved entrepreneurs. The SBA Microloan program caps at $50,000 and works through intermediary nonprofit lenders who often accept credit scores in the 575–620 range. Processing is slower, but terms are reasonable for the risk profile.

Finding a cosigner with stronger credit can open doors to better rates. This is a personal decision with real relationship implications, but from a pure financing standpoint, it’s one of the most effective ways to access lower rates when your personal credit doesn’t qualify on its own.

Building credit strategically before applying is also worth the investment of time. If your timeline permits, 6–12 months of on-time payments on a secured credit card and a small credit-builder loan can move your score meaningfully — often by 50 to 80 points. Patience here can save thousands in interest over the life of your food truck loan.

Explore more about accessible truck options in our guide to affordable food trucks.

Beyond Loans: Grants, Crowdfunding, and Investor Funding

Loans aren’t the only way to fund a food truck, and the smartest financing strategies often combine multiple sources to reduce total borrowing and distribute risk.

Small business grants are essentially free money — no repayment required. The challenge is competition and eligibility requirements. The SBA doesn’t offer direct grants for food trucks, but several programs target food entrepreneurs. Kiva offers 0% interest microloans up to $15,000 through a crowdfunding model. Various state and local economic development agencies run grant programs for small food businesses, particularly those owned by women, minorities, or veterans. Our food truck grants guide covers current programs in detail.

Crowdfunding through platforms like Kickstarter or Indiegogo has launched hundreds of food trucks. The approach works best when you have a compelling concept, a strong local following, or a unique story that resonates with backers. Successful food truck campaigns on average raise between $5,000 and $30,000. The tradeoff is time: building and marketing a crowdfunding campaign takes significant effort, and there’s no guarantee you’ll hit your target.

Private investors are another avenue, specifically if you can demonstrate a viable business model with clear ROI projections. Angel investors or even friends and family might provide capital in exchange for equity or a revenue-sharing arrangement. The data consistently shows that a thorough business plan with detailed financial projections is essential for any investor conversation — they want to understand your break-even timeline, your competitive positioning, and your exit or repayment plan.

When I scaled from one truck to our fleet, the second truck was financed through a combination of equipment financing and reinvested profits from the first truck. The third used a different mix entirely. There’s no single right answer — the best funding structure depends on your specific situation, timeline, and risk tolerance.

For deeper thinking on whether outside capital makes sense for your operation, see our food truck investment analysis.

Lease-to-Own vs. Buying: When Each Makes Financial Sense

Lease-to-own and traditional purchasing represent fundamentally different financial strategies, and choosing the wrong one based on monthly payment alone can cost you thousands over the life of the agreement.

Buying with a loan means you build equity from day one. Once the loan is paid off, the truck is yours free and clear — you can customize it however you want, and you can sell it to recoup some of your investment if you exit the business. The downside: higher down payment requirements (typically 10%–20%) and a larger monthly commitment during the loan term.

Lease-to-own keeps your initial cash outlay lower — sometimes as little as the first and last month’s payment. You get a truck on the road faster with less capital. Many lease-to-own programs include a $1 buyout at the end of the term, meaning you own it after the final payment. The downside: total cost is typically higher than purchasing with a loan when you add up all payments, and you may have restrictions on modifications during the lease period.

There’s also a tax angle worth noting. Under Section 179, food truck owners who purchase equipment may be eligible to deduct the full cost in the year of purchase rather than depreciating it over time. Lease payments may also be deductible as a business expense, but the tax treatment differs. This is one area where I’d strongly recommend talking to an accountant — the specifics depend on your business structure, income level, and state tax rules.

When I ran the numbers comparing a 5-year equipment loan at roughly 10% APR versus a lease-to-own arrangement on a comparable truck, the loan saved approximately 8% to 12% in total cost. But the lease required significantly less cash upfront. For an operator with limited savings and strong projected revenue, the lease made the math work despite the higher overall price tag.

Common Mistakes That Get Food Truck Loan Applications Rejected

Having reviewed loan applications from both sides of the desk — as a banker processing them and as an operator submitting them — I’ve identified the most common reasons food truck loan applications fail, and most of them are entirely avoidable with proper preparation.

Unrealistic revenue projections are the number one killer. Lenders see hundreds of food truck applications, and when yours shows $25,000 per month in revenue for a single truck operating 5 days a week in a small market, it signals that you haven’t done your homework. Conservative, well-researched projections are far more credible — and in my experience, operators who underestimate revenue in their applications typically overperform once they’re running, which builds lender confidence for future financing.

Incomplete documentation causes avoidable delays and outright denials. Missing a single tax return or providing bank statements that don’t cover the required period gives lenders an easy reason to pass. Specifically, prepare every document listed in your lender’s requirements and double-check dates and completeness before submitting.

Requesting the wrong loan type wastes everyone’s time and signals poor preparation. If you need $30,000 for a used trailer, applying for a $200,000 SBA 7(a) loan tells the lender you haven’t researched your options — matching the loan type to your actual need is one of the simplest ways to improve approval odds.

No business plan — or a generic template plan is a disqualifier for most lenders. Your plan should demonstrate specific knowledge of your local market, your concept’s competitive advantages, and your operational costs. Template plans with placeholder text are obvious to reviewers and reflect poorly on your overall preparation.

Ignoring your debt-to-income ratio is a mistake I see repeatedly. Even with a strong credit score, if your existing debt obligations consume too much of your income, lenders won’t approve additional debt. The numbers tell a different story than credit score alone — paying down existing balances before applying can make the difference between approval and rejection.

Applying to only one lender guarantees you’ll overpay. Rates, terms, and fees vary significantly across lenders, and failing to compare at least three options means you’re leaving money on the table without even knowing it.

Putting It Into Practice

📅 Today: Check your personal credit score for free (Credit Karma or your bank’s app) and list all existing debts with current balances and monthly payments. Calculate your debt-to-income ratio.

📅 This Week: Create a detailed budget covering the truck, equipment, permits, insurance, initial inventory, and 3 months of working capital. Get written quotes from at least 2 truck vendors. Begin drafting or updating your business plan with realistic revenue projections.

📅 This Month: Submit pre-qualification applications to 3–4 lenders (SBA lender, equipment financing company, and at least one alternative lender or CDFI). Compare APR, total cost of borrowing, and funding timelines before signing.

Tools You’ll Need: Credit monitoring service, business plan template, vendor quote documents, loan comparison spreadsheet, personal financial statement form.

FAQ: Food Truck Loans

How hard is it to get a loan for a food truck?

Difficulty depends primarily on your credit score, time in business, and the loan type you pursue. Borrowers with FICO scores above 680 and at least 1–2 years of business or food industry experience will find the most options available. Startups with scores between 600 and 680 can typically qualify through equipment financing or microloans. Below 600, the options narrow but don’t disappear — CDFIs and nonprofit lenders work specifically with underserved borrowers.

How much is a loan for a food truck?

Food truck loans typically range from $5,000 for basic equipment upgrades to $200,000 for a new custom-built truck with full kitchen buildout. The most common loan range for a single truck falls between $50,000 and $125,000, covering the vehicle, equipment, and initial setup costs.

What credit score do you need to buy a food truck?

Most traditional lenders look for a minimum of 650, with the best rates reserved for scores above 700. Equipment financing lenders may go as low as 600 because the truck serves as collateral. Some CDFI and nonprofit microlenders have no minimum score requirement, though rates will be higher to offset the increased risk.

Can I get a food truck loan with no money down?

It’s rare but possible through certain equipment financing programs or lease-to-own arrangements. Most lenders require 10% to 20% down. A higher down payment reduces your monthly obligation and on average unlocks better interest rates, so even if zero-down is available, putting money down typically makes financial sense.

How long does it take to get approved for a food truck loan?

Timeline varies dramatically by loan type. Online lenders and equipment financing companies may approve within 1–3 business days. SBA loans typically take 30–90 days due to the extensive documentation and review process. Microloans from nonprofit lenders usually fall somewhere in between, averaging 2–4 weeks.

Do food trucks qualify for SBA loans?

Yes. Food trucks qualify under both the SBA 7(a) program and the SBA Microloan program. The truck and equipment are considered eligible business assets. As of 2025, collateral is now required for loans above $50,000 and guaranty fees have been reinstated. Verify current citizenship and residency requirements directly with the SBA, as these rules are being updated.

Can I use a personal loan to buy a food truck?

Technically yes, but it’s typically not the optimal path. Personal loans carry higher interest rates than equipment financing on average, don’t build business credit, and offer shorter terms. The one scenario where a personal loan may make sense is for a very small purchase — under $10,000 — where the simplicity of the application process outweighs the rate difference.

How often do food trucks fail?

Industry data suggests roughly 10% to 30% of food trucks cease operations within their first three years, though precise failure rates are difficult to verify because many closures go unreported. The most common reasons are poor location strategy, insufficient working capital, and underestimating operating costs — all factors that proper planning and right-sized financing can mitigate. For a realistic look at earnings, see our analysis of whether food trucks really make money.

Choosing the Right Financing Path for Your Food Truck

Key takeaways:

- Equipment financing (typically 5%–20% APR) offers the most cost-effective path for truck purchases, since the vehicle serves as collateral and reduces lender risk.

- SBA 7(a) loans offer rates of 11%–16% and terms up to 10 years — but expect 30–90 days for approval and collateral requirements on loans above $50,000.

- Your monthly loan payment should stay below roughly 15%–20% of projected gross revenue to maintain healthy operating margins.

- CDFI lenders accept FICO scores as low as 600, and some work with borrowers who have no FICO score at all — rates run higher (14%–17%) but access is real.

- Crowdfunding campaigns for food trucks typically raise $5,000–$30,000, enough to reduce your loan amount but unlikely to replace financing entirely.

- Comparing at least 3–4 lenders before committing is one of the simplest ways to save thousands over the life of your loan.

Your next steps: Download our Food Truck Loan Application Checklist to organize your documents before applying. If you’re evaluating specific grant programs, our food truck grants guide covers current options. For lenders that specialize in mobile food businesses, our food truck loan comparison breaks down what each offers.

For the complete picture of funding your food truck business — from calculating total costs to choosing a financing structure — return to our Food Truck Financing hub.

— Marcus Reyes

The most common financing mistake isn’t choosing the wrong loan type — it’s not running the numbers before you commit. Every lender will tell you what they can offer. It’s your job to calculate what you can actually afford.